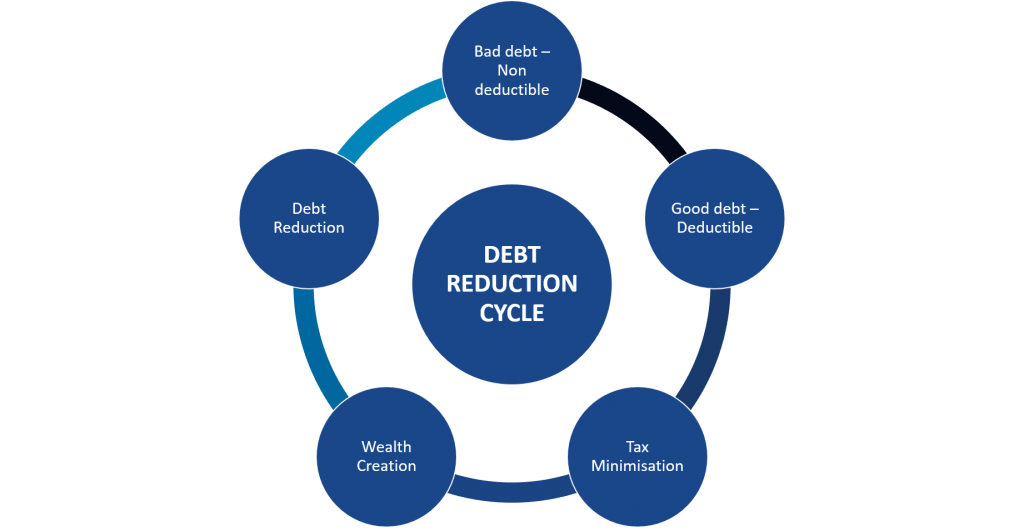

Debt recycling is borrowing against the equity in the home for investment purposes and applying the net income from the investments (plus any cash surplus) to replace bad debt with good debt. This ‘recycles’ debt to assist in accelerating wealth creation.

This strategy is appropriate for clients who have a home loan and want to accelerate their wealth creation using home equity and gearing. The client uses some of the available equity to take out an investment loan and repeats these steps at the end of each year until the home loan is paid off:

- The client invests borrowed money into growth assets such as shares or managed investments

- The client then uses the investment income and tax savings plus surplus cash flow to reduce their outstanding home loan balance

- At the end of each year, the client borrows an amount equal to what they’ve paid off their home loan

- The client then uses this money to buy additional investments

As with all strategies, gearing should only be used where the risks have been fully explained and understood by your client.

It may take slightly longer to pay off the home loan, as some of the surplus cash is used to meet interest costs on the investment loan, which increases over time. However, the client begins building their investment portfolio sooner. Provided the client’s after-tax return from their investments is greater than the interest costs of the loan, it’s likely to be more effective to reinvest surplus cash flow than use it to pay off the investment loan as the interest is tax-deductible.